Property Depreciation explained

When it comes to investments and assets, depreciation is very common. It happens to cars, watches, and, yes, even investment properties.

In basic terms, depreciation represents how much an asset decreases in value due to time, obsolescence, or wear and tear.

But how do investment properties depreciate? Aren’t property prices soaring? If I purchase an investment property, its value should be going up, not down, right?

Well, yes, and chances are if you’re fortunate enough to own an investment property or are looking at getting into the investment property game, your investment property is going to grow in value when compared to when you first purchased it. But property depreciation, refers to the building and its contents, not the investment itself. The bottom line is that property depreciation is a tax term more than a property term.

When lodging your tax return, you can claim a deduction on an investment property’s structure, as well as any permanent equipment and items in the property (such as, ovens, air conditioner, etc). Investment property owners will then pay less tax on the property.

How does it work?

The ATO considers the investment property a purchased building and applies the capital works deduction for depreciation. There are two ways to figure out the deduction:

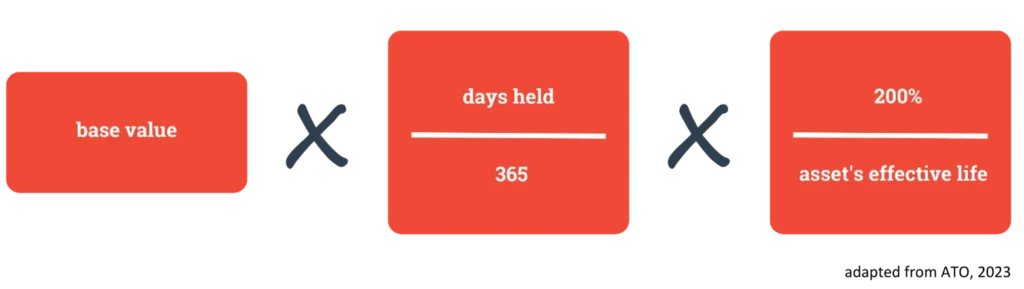

Diminishing value method: The diminishing value uses a constant decline rate annually to determine the depreciated value. If you purchased an asset after May 10, 2006, the below calculation can be used.

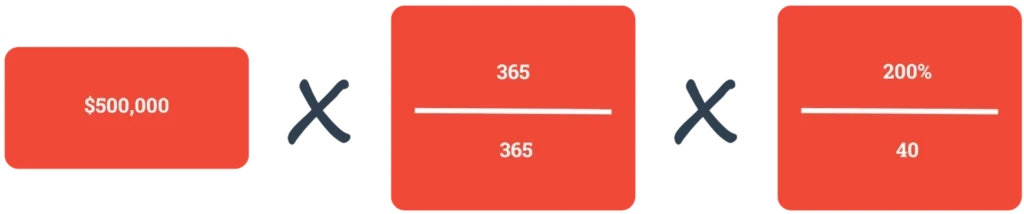

For instance, if the property’s base value is $500,000 at purchase price, and it’s intended to have an effective life of 40 years, the claim for the first year is $25,000.

The property’s value for the second year would then be the purchase price minus the deduction. Meaning year 2 to year 3 the base value would be $475,000. This assumes the property will depreciate more in its early years and less later in the property’s life.

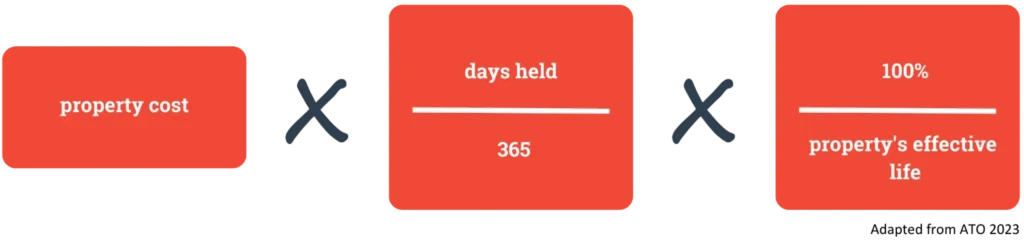

Prime cost method: The prime cost method is a ‘straight-line method’, meaning a consistent decrease over the life of the loan.

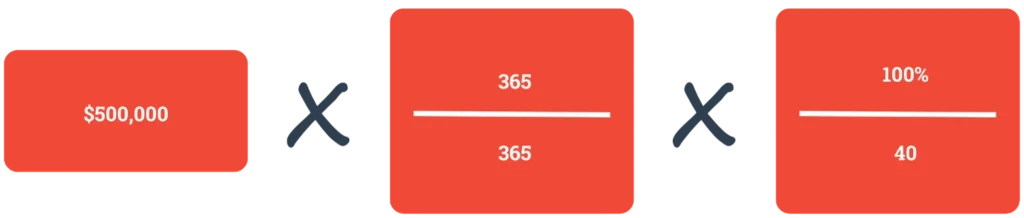

In this case, your property would see the same deduction annually, meaning the deduction doesn’t alter over the full life of the loan. Using this equation, you would see a 2.5% deduction of the original cost annually. The depreciation that could be claimed would be $12,500.

Keep in mind these two methods are rules of thumb only, and we recommend seeking assistance from a qualified tax professional or accountant for accurate deduction estimates.

Why should I deduct my property depreciation?

Claiming tax deductions based on your asset’s depreciation can reduce the tax you need to pay on the property. The building will likely sustain wear and tear over its life, meaning you shouldn’t have to pay the same amount of tax on it year in and out.

If you’re in the market for an investment property, our team can assist with finding you a suitable loan or consolidating your debts. We’re here to help you every step of the way!

Disclaimer:

This article is written to provide a summary and general overview of the subject matter covered for your information only. Every effort has been made to ensure the information in the article is current, accurate and reliable. This article has been prepared without taking into account your objectives, personal circumstances, financial situation or needs. You should consider whether it is appropriate for your circumstances. You should seek your own independent legal, financial and taxation advice before acting or relying on any of the content contained in the articles and review any relevant Product Disclosure Statement (PDS), Terms and Conditions (T&C) or Financial Services Guide (FSG).

Please consult your financial advisor, solicitor or accountant before acting on information contained in this publication.

Proudly Part Of

The Money Quest Group (MQG) is one of Australia's leading boutique mortgage broking businesses, with a network of more than 600 brokers nationwide. Known for their exuberant culture and superior support, MQG provides brokers access to a range of financial products from more than 60 lending institutions and suppliers, and exclusive access to in-house benefits and services.

© 2017-2025 MoneyQuest Australia Pty Ltd, Australian Credit Licence 487823